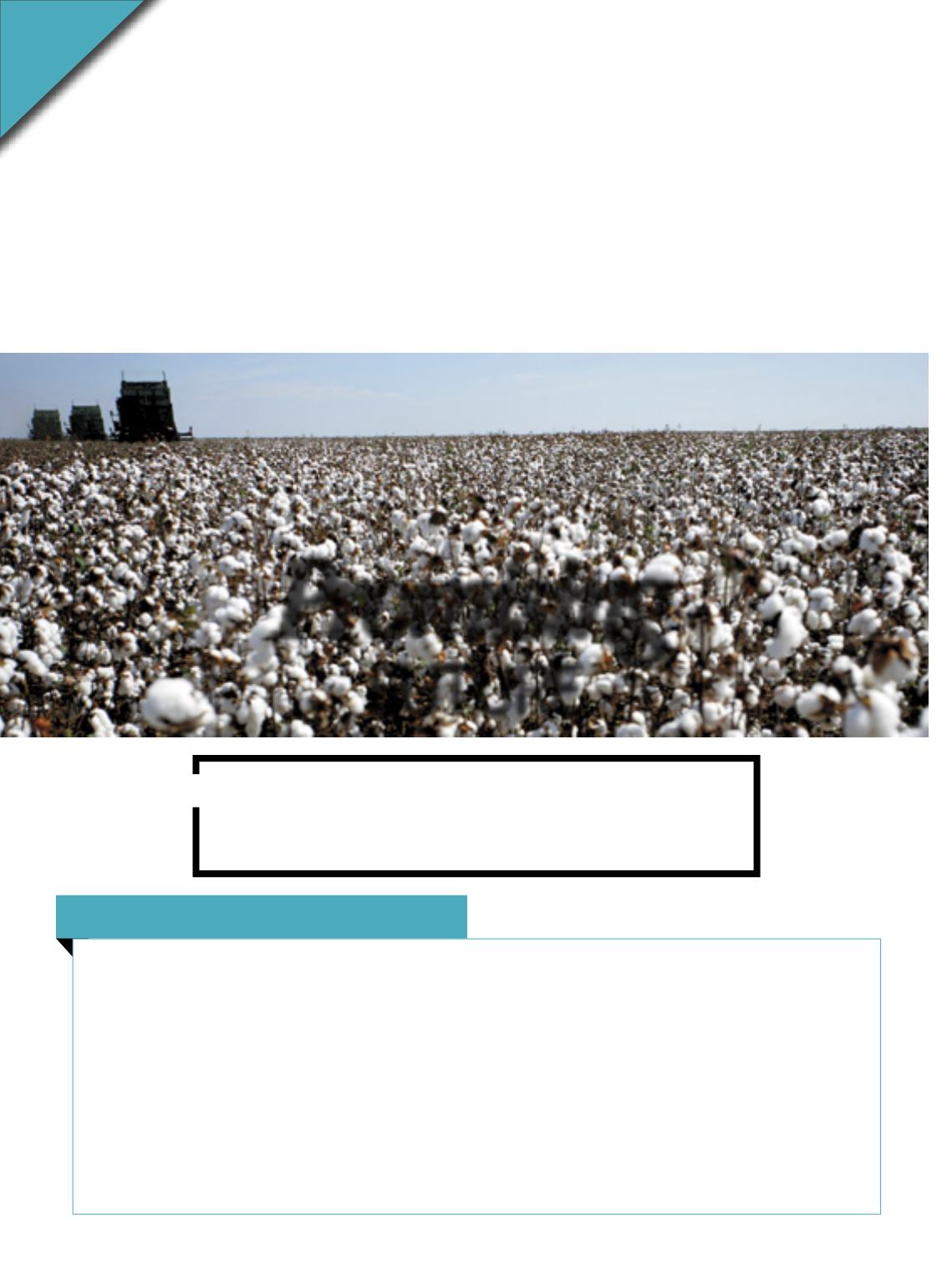

I

f the expectation is for remunerating

prices for the cotton supply chain in the

commercialization of the 2016/17 crop,

whose prices went up 60% up to June,

when harvest started, they still remain

below desirable levels. “Despite the peak in

the futuresmarket, at theNewYorkStockEx-

change,inMay,duringsomedayswheninter-

nationalquotesreachedUS$0.87perpound,

there is need for people to keep their eu-

phoria under control and refrain from imag-

ining that prices will naturally climb to one

dollar per pound, as some market agents

had suggested”, warns Élcio Bento, analyst

with Safras &Mercado. Bruno Nogueira, an-

alyst with the National Food Supply Agency

(Conab), agreeswith this position.

Both of them believe that the price lev-

els throughout the international commer-

cial season that extends from August 2017

to July 2018 should remain above US$ 0.80

per pound, consolidating a recovery po-

sition against the prices practiced in the

two previous seasons. “Although the price

peaks reached at the futures market have

had an important role as a hedging strat-

egy and closed business deals, the pres-

ent commercialization parameters point

to lower averages as soon as the new Bra-

zilian crop reaches the market, in June,

and the North-American crop, in August,

Nogueira comments.

Some numbers, however, are positive.

Bymid-May, more than 65%of the 2016/17

cotton crop inMato Grosso had been nego-

tiatedinadvance,whileinthepreviousyear

the volume had reached 50%. “With indi-

cations for a crop failure, the cotton farm-

ers remained rather restrained”, says Él-

n

n

n

Impact on stocks

As the majority of the cotton in Mato Grosso, and from a big number of other Cerrado regions, is concentrated on the second

crop, after soybean harvest, the fiber could make a difference in this growing season. “Considering the international soybean

prices, it is possible that lots of farmers achieve with cotton their goal in obtaining profits from the grain”, recognizes Élcio Ben-

to. According to the analyst, adding the sales of fiber to the sales of seed in late May, cotton achieved positive profitability of 6%

over the production costs in Mato Grosso, while soybean and corn showed a negative performance. “While the margin is not the

desired one, at least it is the one that brings in higher remuneration”, he explains.

While the Brazilian domestic market managed to keep prices remunerative, the relation with the international trade at the

peak of the fallowperiodwas disadvantageous. “Brazil lost competitiveness in the first half of the year. The smaller crop adverse-

ly affected supply and the domestic market had to pay higher prices to fulfill their demand”, Bento stresses. “From 932 thousand

tons exported in the previous year, we are now achieving something about 600 thousand tons”. As soon as harvest starts, none-

theless, prices that remained 3% above international quotes, should drop and seek parity. With the domestic production cost

ranging from R$ 2.50 to R$ 2.60 per pound, a positive margin is not out of the question.

Expectation is for profitable trade

throughoutthe2017/18commercialyear,witha60percent

increaseinsales,butdistantfromtheUS$1perpound

Promising

future

Sílvio Ávila

52