46

B

razil’s most popular fruit, the or-

ange, of which the Country is the

leading global producer, along

with the juice, dropped consider-

ably in production over the past

years and, in the 2016/17 growing season

(June through July), should register further

declines.Intheso-calledCitrusBelt(SãoPau-

lo andTriânguloMineiro), which concentrates

twothirdsofthetotal,thevolumeislikelytogo

down 18.7%, the smallest in 28 years, accord-

ing to an estimate by the Citriculture Surveil-

lance Fund (Fundecitrus), in December 2016.

For the next season, the segment anticipates

a possible reaction, although supply is sup-

posed tocontinue tight.

The explanation for the recent result lies in

poor “fruit setting” in themajority of the citrus

belt producing regions, by virtue of the abnor-

mally high temperatures in the processing pe-

riod. Furthermore, according to an analysis by

the Center for Applied Studies on Advanced

Economics (Cepea), of the Luiz deQueiroz Col-

legeof Agriculture (Esalq), linked to theUniver-

sityof SãoPaulo (USP), the reduction in thecit-

Due to the smaller production in Brazil and in the United

States, prices of both the raw material and the industrial prod-

uct registered expressive increase at home and abroad, ac-

cording to Cepea sources. In the partial average of the season

between July and December 2016, the price of sweet and late-

maturing oranges reached R$ 22.21 per 40.8-kilogram box, at

the processing plants, up 79.2% from the average of the same

period in 2015. Juice prices at the New York Stock Exchange, in

late 2016, fetched upwards of US$ 3,000 a ton.

Forthe2017/18growingcycle,theindicationascertainedbythe

CenterofAppliedStudies,inearlyJanuary2017,pointedtoincreas-

es in production. Within this context, the contribution is supposed

tobecomingfromthefruitingbudsandtheirsatisfactoryblossom-

ing, alongwithaverageor aboveaverage rainfall,mildclimate con-

ditions favoring the fruit setting process, besides a resumption of

investments in cultural practices, driven by the higher prices. The

main producing region is again supposed to reach results of ap-

proximately300millionboxes,against244millionestimatedforthe

previous season. However, the volumes will not be big enough to

bringorange juice stocksback to the technical balance.

n

n

n

Willingness to invest

Productionoforanges

andjuicesinBrazil,

leadingproducer,

droppedconsiderably,

pricesarehighanda

resumptioninthenew

cycleisexpected

Renewing

energy

rusparkoverthepastyears,stemmingfromthe

price crisis; limited investments by the farmers

andtheoutbreaksofthe“greening”diseaseac-

countforthesmallervolumeproduced.

As a result, the companies’ closing stocks

could be reduced to almost zero at the end of

the season. The volume of stocked juice an-

ticipated by the National Association of Citrus

Juice Exporters (CitrusBR) for that moment, in

June2017,issupposedtoremainat2thousand

tons, the lowest level in history and way be-

lowtheamountconsideredtobestrategic,300

thousand tons. Leading supplier of the prod-

uct,with97%destinedforabroad,andrespon-

sibleforabout70%ofthetotalvolumetradedin

theworld, Brazil supplies themarket and, from

July to December 2016, the shipments abroad

reachedthesamevolumeofthe2015period.

In the 2016 civil year, exports of Brazilian

orange juice were slightly up (4%) from 2015,

andinthefirstsixmonthsofthe2016/17grow-

ing season the numbers suffered no changes.

The mainmarket is the European Union, and

its purchases increased slightly in 2016, while

the partial numbers of the new cycle went

down. In themeantime, the shipments to the

UnitedStates,secondbiggestclientoftheBra-

zilian product and second-largest global pro-

ducer, now dealing with a smaller crop, went

up19%duringthefirsttwoquarters.

Inor Ag. Assmann

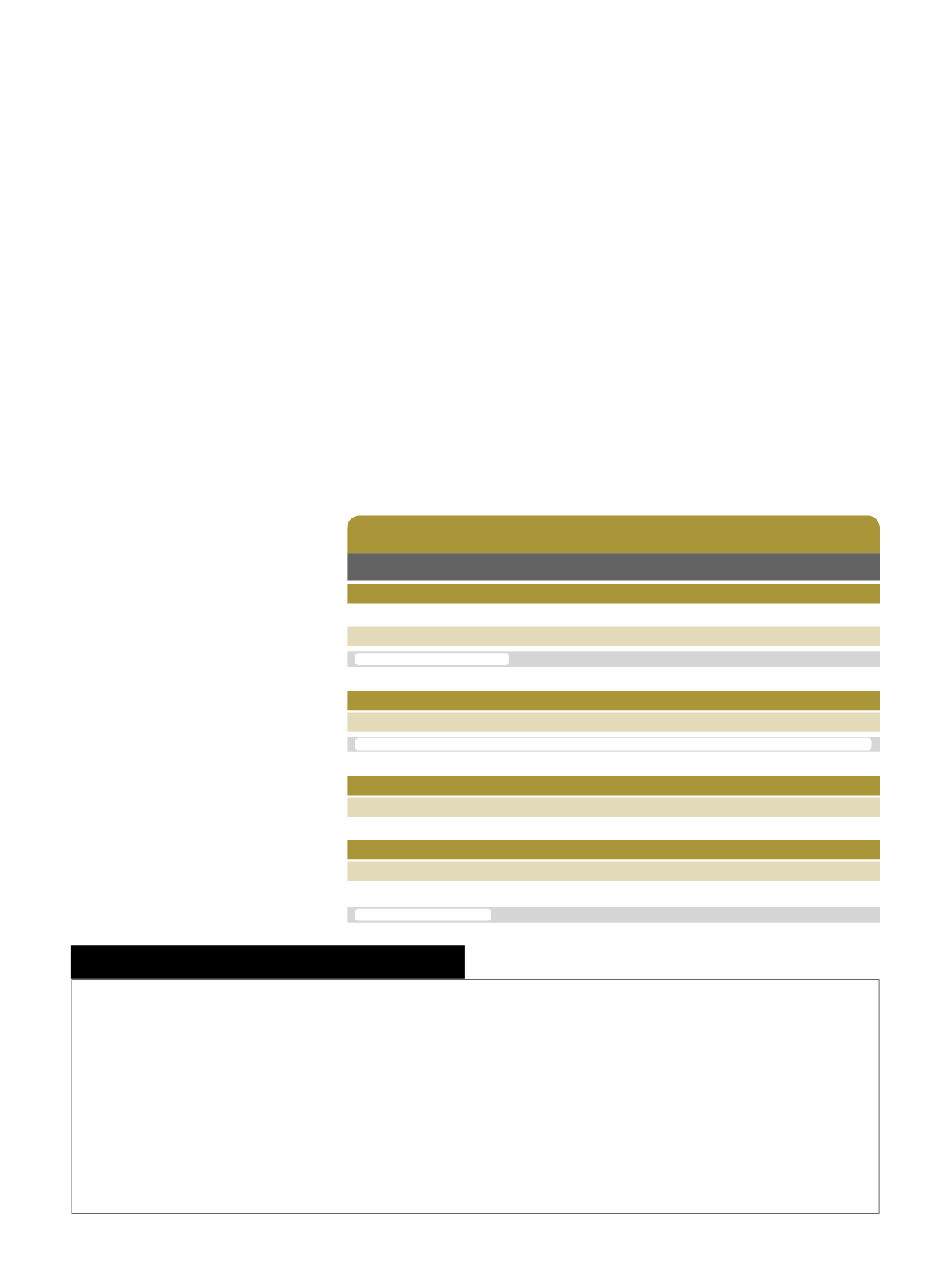

Números da laranja no Brasil

CAMPEÃDOSPOMARES

Orchard leader

Exportaçãode sucode laranjadoBrasil

AnoCivil

2015

2016

Volume (T de FCOJ equivalente)

1.038.466

1.080.448

Receita (US$mil)

1.764.710

1.800.460

Parcial safra (Julho-Dezembro)

2015/16 (2015) 2016/17 (2016)

Volume (T de FCOJ equivalente)

475.406

474.916

Receita (US$mil)

776.261

831.848

Fonte: Secex-MDIC/CitrusBR.

Safra

2015

2016

Área (ha)

665.174

667.529

Produção (t)

16.746.247

15.983.273

Fonte:IBGE/Dezembrode2016

CinturãoCitrícola (SãoPauloe TriânguloMineiro)

Safra

2015/16

2016/17

Produção (t)

12.266.520*

9.963.360**

Fonte: Fundecitrus/Dezembro 2016 (* 300,65 milhões de caixas de 40,8 kg/** 244,20 milhões de caixas de 40,8 kg)